ASteve Sosnick, the chief market strategist at Interactive Brokers, referred to financial market activity in May as “the Everything Rally.” That’s not a bad way to frame what happened last month.

At the start of the month, investors were confronted with an unsigned Iran peace deal, oil above $100, inflation at a three-year high, a brand-new Federal Reserve chair, and a 30-year Treasury yield touching its highest level since 2007.

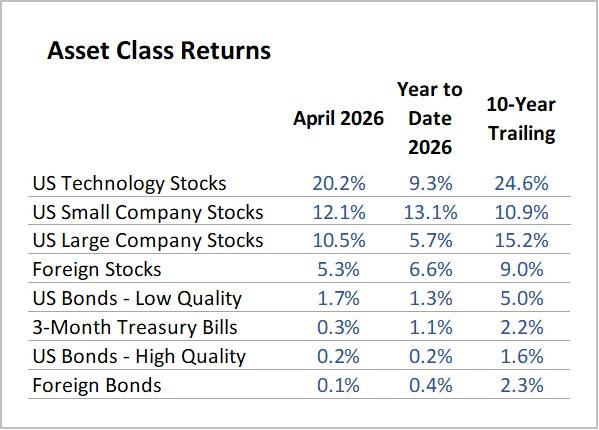

May closed with Technology sector posting another double-digit monthly gain. The S&P 500 index of large company US stocks rose 5.3% and closed at record highs on 11 days during the month. Foreign stocks gained more than 2.4%, and bond indices (despite large intra-month swings in yields) registered modest positive returns.

May was defined by three themes: the Iran war and its economic consequences; AI delivering broad-based, positive revenue trends in the technology sector; and a bond market that tested investor nerves.

The Iran War — Deal Always “Just Around the Corner”

The U.S.-Iran conflict is now in its fourth month. The Strait of Hormuz remained largely closed to commercial traffic, with only a handful of ships transiting daily versus 120 before the war.

Oil prices swung dramatically on diplomatic signals: Brent crude peaked near $126 in late April, fell toward $87 by month-end, then traded at various points in between as headlines shifted from hope to frustration and back again.

The month’s diplomatic arc was a recurring pattern: a constructive signal would arrive, sending oil sharply lower and stocks higher — only to be followed by a complication. By month-end, the memorandum of understanding between the US and Iran remained unsigned, and June opened with the same central question May had posed: when will a deal be signed?

The economic consequences of the conflict were visible throughout the month. Inflation hit 3.8% year-over-year — its highest since 2023 — driven heavily by energy. National average gas prices remained above $4.50 per gallon for most of the month.

And Goldman Sachs and Barclays both cautioned that even if the Strait fully reopened tomorrow, global oil inventories are so depleted that prices likely would normalize only gradually, not immediately.

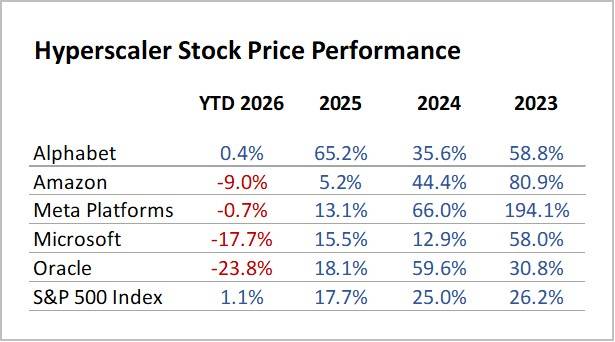

Artificial Intelligence Delivers Positive Revenue Trends

April validated that AI is driving positive financial results for chip makers. May confirmed that AI demand is broadening into other areas of the technology ecosystem.

Some examples of how AI-driven demand is benefiting tech companies:

- Dell Technologies, which many folks associate with personal computers, reported AI server revenue up 757% year-over-year, a record $51.3 billion AI order backlog, and raised its full-year revenue forecast by roughly $27 billion.

- Cisco, another “old-line” technology-focused company, known for its networking gear that supports internet activity, raised its full-year AI order guidance to $9 billion — nearly double what it had guided just one quarter earlier.

- Nvidia, the new tech standard bearer that designs chips, and also hardware networks to power data centers as well as specialized software, reported $81.6 billion in quarterly revenue — up 85% year-over-year — and guided its next quarter to $91 billion.

- Cerebras Systems, which delivers supercomputer systems and cloud-based services, listed its shares through the largest tech initial public offering (IPO) since Uber went public in 2019, saw its shares surge 68% on the first day of trading.

The broader AI narrative for the month was captured well by one market analyst: “We started with chips and memory, but it’s really now about the broad AI infrastructure stack.”

And more AI-related activity is in store for investors in the months ahead, with SpaceX, Anthropic (maker of Claude) and OpenAI (maker of ChatGPT) all expecting to list their shares through IPOs and being trading on stock market exchanges later this year.

The Bond Market’s Warning

Not everything pointed straight up in May.

The bond market delivered a warning mid-month that temporarily interrupted the equity rally. The 30-year Treasury yield approached 5.2% in mid-May – its highest level since 2007, before the financial crisis – and the 10-year Treasury yield approached 4.7% (though bond yields did decline in the back half of May).

The main driver of higher yields was the Iran war’s inflationary impact on energy prices globally. The practical consequence for US households: 30-year fixed mortgage rates climbed back to 6.68%, putting further pressure on an already-stalled housing market.

Adding to the complexity, Kevin Warsh took over as Federal Reserve Chair on May 15, inheriting a divided institution with inflation running well above its 2% target.

The probability of a Fed rate hike in 2026, which was essentially zero a month ago, climbed as high as 45% during the month. Warsh’s first formal interest rate policy decision comes June 16.

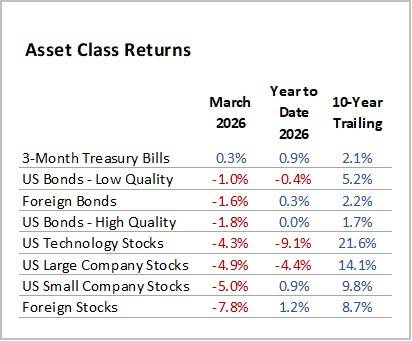

Despite the swings in yields, benchmark US bond indices delivered positive returns in May. High quality bonds returned 0.3% for the month, and low quality bonds rose 0.5%.

As June begins, the questions that defined May remain open. The Iran deal is unsigned. Inflation remains elevated. The new Fed chair faces his first policy decision with rate-hike odds that would have seemed unthinkable a few months ago.

And yet the stock market enters June at all-time highs, with US Large Company Stocks up 11.2% for the year and Foreign Stocks up 9.1%. Whether the optimism that has driven the fourth consecutive year of stock market gains (so far) proves durable is the central question for the months ahead.

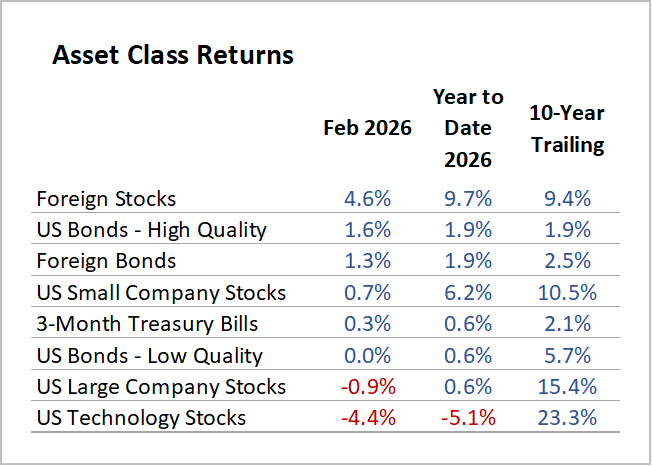

Here are results for May and 2026 Year-to-Date, compared to longer-term annualized returns (10-Year Trailing):

Note: YTD 2026 as of 5/31/2026; Source: Morningstar

-RK