On Wednesday, May 3, the Federal Reserve delivered the 10th interest rate hike since beginning its fight against inflation in earnest in March 2022. The latest action pushed the Fed Funds short-term interest rate above 5% for the first time in 15 years.

In his press conference following the rate hike announcement, Fed Chair Jerome Powell indicated that he expects the economy to slow down and inflation to continue to decline in 2023.

This implies that the Fed likely will be able to take a break from boosting short-term interest rates soon, and that we may be in for an extended period of Fed inaction.

In this note I share some perspective on what a pause after a period of interest rate increases means for investors holding bonds and bond funds.

In the months and quarters following the pandemic, Wall Street people often used the acronym TINA (There Is No Alternative) when referring to stocks.

After interest rates dropped to the floor in 2020, and stayed there for some time, bonds offered little by way of returns, while many stocks and stock funds paid dividends and appreciated in price, especially in 2020 and 2021.

In 2022, the financial markets turned from TINA to TONR (There’s Only Negative Return) as investors suffered through high inflation, rising interest rates, and stock and bond bear markets.

However, the change in the interest rate environment, which started in 2021 and accelerated in 2022, brought a benefit, by way of higher yields, that improves the long-term outlook for bond fund holders.

In 2023, we’ve got BANANA – Bonds Are Now A Nice Alternative. In some cases, bonds and bond funds now present compelling yields with satisfactory total return potential.

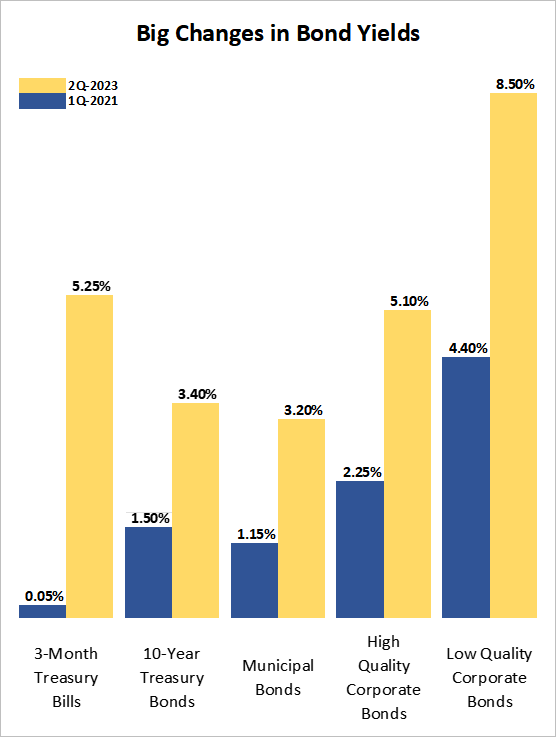

The chart below compares where yields were for different types of bonds two years ago (in early March 2021) with where yields are today, following a period of inflation-fighting by the Federal Reserve.

The sharp yield increase resulted in a steep decline in bond prices in 2022. What does this mean for investors going forward?

DoubleLine, the bond fund manager, has done some research on this topic. Their analysis shows that the prospects for positive returns from bond fund holdings, in years following sharp yield rises (and corresponding price drops) is quite good.

The average price of bonds in the Bloomberg US Aggregate Bond Index (a broad measure of High Quality Corporate and Government bonds) going back to its inception in 1977 is $100. Today, the average price is in the low $90s.

According to DoubleLine, investing in High Quality bonds when the average price of the index is between $90 – $100 has typically meant returns of between 5% – 10% during the next 12 months. In years following sharp yield increases, bond returns historically have been positive.

While 2022 was painful for bond fund holders, the next several years (assuming the average bond price remains below $100) may be more pleasurable for investors who have significant bond allocations in their portfolios.