The financial markets have been influenced by two major themes in 2023.

For stocks, Artificial Intelligence (AI) has captured the imagination and the dominance of large technology companies has been a driving force.

For bonds, concern about inflation and the Federal Reserve’s reaction to it has been behind the persistent rise in interest rates. Read on for a discussion of what these themes mean for your investments.

Stocks: Less Magnificent

The seven largest technology companies in the US have been cheekily labeled the Magnificent Seven. Some may recall the film from 1960 by the same name, a Western about seven American gunslingers.

The 21st century capital markets version casts Alphabet (aka Google), Amazon, Apple, Meta Platforms (aka Facebook), Microsoft, Nvidia, and Telsa as the lead characters.

Year-to-date, the M7 are up about 80% on average. This compares to a gain of 10.6% for the S&P 500 Index, which is the benchmark for the 500 largest companies in the US.

Over the past five years, the M7 surged more than 200%, compared to about 27% for the S&P 500 (statistics courtesy of Clearnomics). Also worth noting is that the M7 comprise nearly 30% of the S&P 500 index.

Another way to think about the M7 phenomenon: if all the stocks in the S&P 500 were given the same weight – equally weighted, instead of weighted by the market capitalization, or relative size of each company’s stock – the stock market performance thus far for 2023 would be negative 2.5%. Which means that, on average, it really hasn’t been a great year for stocks.

As you might expect, legions of analysts and strategists have been diligently analyzing and prolifically prognosticating about this M7 phenomenon. In summary, the message from Wall Street: AI is a special technological development that will change the world.

These are great companies that make ingenious products, and they likely will continue to generate gigantic revenues and prodigious profits for the foreseeable future. However, “greatness” and “ingenuity” appears to be reflected in the M7 stock prices – and then some.

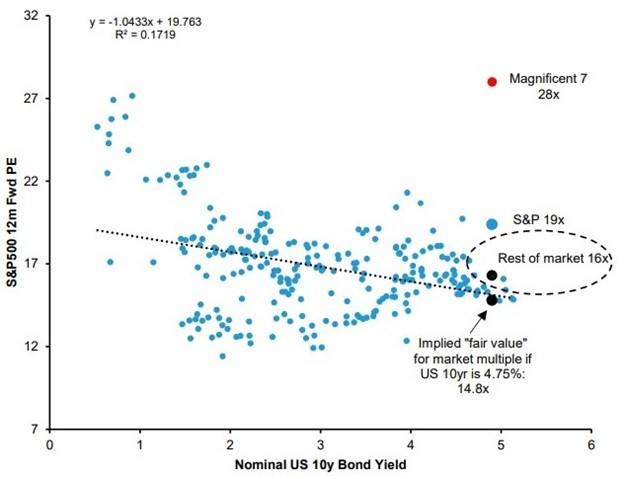

The chart below is an example of wonky Wall Street stock market research (this one produced by Richard Bernstein Associates and reproduced by Bloomberg). At a quick glance it might be hard to decipher, but upon closer study it highlights three important points about today’s stock market:

- Big tech stocks (M7) are quite expensive relative to other stocks (red dot)

- Non-tech stocks are much more reasonably priced (black dot)

- Interest rates affect what people think the “fair value”, or reasonable price, should be for stocks (dotted line thru the blue dots)

A few additional notes on the above chart:

- About the P/E: S&P 500 12-month Forward Price / Earnings Multiple (vertical axis): The Price / Earnings Multiple (P/E) is one standard metric used by analysts when trying to determine the relative value of a stock. It is the price paid for each $1 of earnings. Based on years of historical data, paying about $16 per share for each dollar per share of earnings a company produces is viewed as a reasonable price, or fair value.

- About Fair Value: The idea of fair value, or the reasonable price to pay for stocks, depends upon what part of the market you’re looking at. Faster-growing segments, like technology, command a premium to slower-growing areas, like utilities. Fair value also moves around as interest rates change.

- Interest Rates & Stock Prices: Last year, when interest rates were 2%, the P/E for the S&P 500 Index was around 18. Today, with interest rates at 5%, the fair value P/E is about 15, and the market trades at 19. This valuation metric says the stock market has some room to fall, given the current level of interest rates.

- Magnificent 7:The P/E for the M7, at 28, is very high relative to the rest of the stock market, so theoretically there’s a lot of room for these seven stocks to fall.

- Non-Magnificent 493:The P/E for the remaining 493 stocks in the S&P 500, at 16, is much closer to fair value, and therefore today is viewed as much more reasonably priced.

- About the Data: Scatter plot uses 20 years of monthly data (from 2003 – 2023)

For investors who have diversified stock allocations – including significant weights to non-technology stocks, small company stocks, and foreign stocks – portfolio performance in 2023 will likely be underwhelming when compared to a benchmark like the S&P 500, or high-fliers like the M7.

While this may be perceived as disappointing, keep in mind that segments of the market fall in and out of favor over time.

Viewed through another lens, stock price declines can present opportunities. Famed stock picker and Newton, MA native Peter Lynch, said in a recent Barrons’s interview: “I love it when stocks go down.”

The bottom line for stock-market investors: the best way to avoid the market-timing pitfall (and the outsized ups and downs that come with it) and enjoy the benefits of long-term, risk-controlled compounding, is to be well-diversified.

What happens in the near term to an individual stock or concentrated group of stocks can be noteworthy and interesting.

But what matters more for your financial wellbeing is how stocks can contribute to your diversified portfolio and your broader financial plan over the long term.

Bonds: 5% is the New 2%

A mere 22 months ago, all Treasury bonds were yielding 2% or less (most much less). The one-year Treasury note yielded about 0.5%. Today, it yields 5.5%. But talking in percentage points can be abstract.

What does the big move in interest rates mean for folks who invest in bonds?

There are two main pieces of the bond puzzle for investors to think about: income and price. Providing concrete examples might be helpful in putting the effects of interest rate increases into perspective.

The Price Piece

You may have a general understanding of the price / yield relationship when it comes to bonds.

You can validate that interest rates have been going up by checking out what’s on offer at your local bank: savings accounts and CDs pay more today, and mortgages cost a lot more.

If you hold individual bonds, or a typical bond fund in your brokerage account or IRA, you’ve probably noticed that the prices are lower today when compared to last month or last year.

The reason is this: as new bonds are issued at current interest rates (which are higher than in the recent past), old bonds, which pay a fixed rate of interest through their coupons, must adjust.

The adjustment mechanism is the price of the bond (or bond fund). The price of old bonds will fall to a level that makes their yield comparable to the yield offered by new bonds.

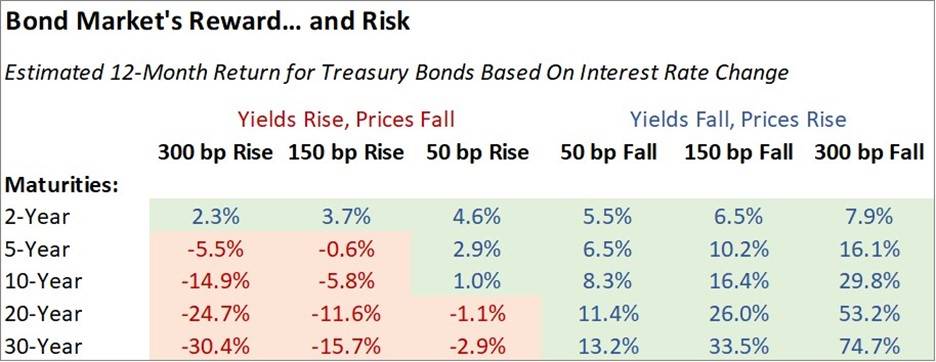

The table below shows how bonds are expected to perform over the course of the next year given various scenarios for changes in interest rates.

Note that bp is ‘basis point’, or 1/100 of a percent. A 300-basis point fall (last column) is a three percentage point decrease from the current level of interest rates. As interest rates fall, bond returns go up. As rates rise, bond returns go down.

One takeaway from the table is that for holders of high-quality short-term bonds (like US Treasuries) it is now difficult to envision an environment where returns for the next 12 months could be negative.

Even if Treasury bond interest rates were to climb to 8% (from today’s 5%), the 12-month return would still be positive for holders of short-maturity bonds. This is because: 1. Short-term bond prices are less sensitive to interest rate movements; and 2. Income from coupon payments more than offsets the negative price adjustment.

For holders of longer-maturity bonds, an interest rate decline would translate to big gains.

But interest rate risk cuts both ways. If rates were to climb by another 1.5 percentage points or more during the next year, it would mean additional losses for holders of intermediate and long-maturity bonds.

The pain for current bond holders has occurred as prices have fallen to adjust to higher interest rates. But the good news is that higher interest rates offer protection against future interest rate increases and price declines. And higher interest rates mean more yield, and therefore more income.

The Income Piece

The pleasure related to bonds is that investors now can reinvest at higher interest rates (compared to the recent past) and therefore earn more money over time.

To put this into perspective, if you invested $100,000 into the 1-Year Treasury in January 2022, you would have collected $500 in interest by the time the bond matured one year later.

Today, if you purchase a one-year Treasury note, you’ll earn about 5.5% in interest, which, on a $100,000 investment, translates to earnings of $5,500. In the span of just under two years, the expected return on short-term Treasuries has increased 11-fold.

This income component of bonds is the straightforward part of the bond puzzle.

The Whole Puzzle

The tough part is that investors holding bonds as part of a balanced portfolio have experienced losses as interest rates climbed. This has unquestionably been painful.

The good news is that you can expect to receive a lot more income from your bond investments, and this income helps to mitigate the downside of interest rate risk.

The bottom line for bond investors: taking some degree of interest rate risk is reasonable for most investors, most of the time. The amount of risk each individual investor should take depends upon their personal circumstances and market conditions.

At this point, given current market conditions, a prudent approach is to err on the side of caution.

Today, one-year Treasury notes yield about 5.5%, and 10-Year Treasuries yield 4.9%. Though the yields are close, the interest rate risk is very different. Some of the better deals, and higher yields, are currently in short-term bonds.

Investors get paid to wait and see how the inflation environment, and the interest rate environment, will unfold in the months ahead.

RK