The war in Iran that began in late February continued throughout March. This put downward pressure on stock and bond prices, as investors worried about how long hostilities would last.

The main concern in March was the inflationary impact of significantly higher oil prices.

The price of oil rose between 50 – 65% in March (depending upon which benchmark oil price is referenced). Many Americans are now paying $4 per gallon of gas.

If the war shows no signs of letting up soon, investors’ concerns will shift to the broader impact on the economy, the likelihood of slower growth, the impending hit to company profits, and the possibility of recession.

We are not at an economic crossroads yet.

The US economy has proven resilient in the face of stress in the energy markets in the recent past.

For example, there was no recession in 2022 when oil prices spiked after war broke out in Ukraine. It’s reasonable to expect that this also will be the case in 2026.

Currently, most forecasters still expect the US economy to expand in 2026 (see the following article) and for company profits to rise.

But if hostilities extend well into the spring, US economic resiliency may be tested further, which would likely mean continued challenges for the financial markets.

The month of March closed with a positive tone with stocks rising 3% on the last day of the month as the US administration signaled its willingness to end the military campaign in Iran.

Investors need to keep in mind that the political and military situation is fluid and volatile; that stocks could decline significantly from today’s levels; and that developments in the Middle East will have a strong impact on the financial markets in the months ahead.

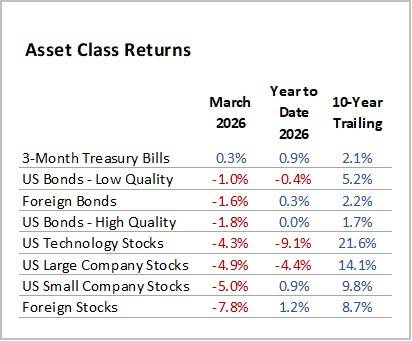

Here are results for March and 2026 Year-to-Date, compared to longer-term annualized returns (10-Year Trailing):

Note: YTD 2026 as of 3/31/2026; Source: Morningstar