At a time when financial markets are experiencing good cheer, many government employees are not.

At 12:01 AM on October 1st, the US government shut down. Many people on Main Street are unsure of what this means. In the following article, we try to bring some clarity to the situation.

Politics Behind the Shutdown

The current dispute revolves around a Republican bill to continue funding the federal government for the next seven weeks while a full-year spending bill is worked out.

Senate Democrats have refused to advance the so-called “continuing resolution” (short-term funding bill) unless Republicans agree to extend certain health care subsidies under the Affordable Care Act that are due to expire soon, and to reverse Medicaid cuts made earlier this year.

Republicans have proposed a clean extension of government spending authority with no strings attached, which runs through the middle of November. Democrats have pushed back on this proposal due to the expiration of healthcare subsidies at year-end.

At least eight Democrats would need to join Senate Republicans to pass a spending bill. So far, three have.

Employment Impact

The shutdown could suspend the work of at least 600,000 government workers out of a total 2.1 million government employees, according to the New York Times. The majority of affected workers come from the Department of Defense.

Federal government employees who are furloughed during a shutdown are guaranteed to receive back pay once the government reopens.

Statements from Trump Administration officials indicate that some non-essential workers could be permanently let go. This would be different from previous shutdowns, and if followed, could have more lasting effects on the US labor market.

Economic Impact

Economists at Goldman Sachs calculate that each week of a government shutdown will shave 0.15 percentage points off quarterly annualized Gross Domestic Product (GDP).

Based on this analysis, it would take about one and a half months of shutdown to shave a full percentage point off quarterly output.

Currently, the quarterly annualized GDP growth rate is about 3%.

Goldman economists are quick to point out that a similar boost to growth in the following quarter (after the government re-opens) is likely, ultimately reversing the negative economic impact.

One concern for retirees likely is: what happens to Social Security payments?

Despite the budget impasse, Social Security recipients will continue getting their monthly payments.

Social Security benefits fall under the category of “mandatory spending.” They have a dedicated, permanent funding source (primarily payroll taxes) and are unaffected by the federal appropriations process.

The staff of the Social Security Administration, however, will be affected.

According to AARP, 88% of the SSA’s 45,600 workforce will remain on the job without pay to maintain essential functions and services. About 6,200 staff are being furloughed.

What the Opinion Polls Say

Recent polling on the topic has consistently shown (according to Goldman Sachs) that more voters are blaming Republicans over Democrats for the shutdown, which thus far has emboldened Democrats to hold their ground and not compromise on their healthcare demands.

Inflection Point

October 15th is a military pay date; if the shutdown goes beyond this day, active-duty military personnel will miss their entire paycheck, which has not happened in past shutdowns.

There is likely little appetite from both parties for this to happen, so 10/15 may end up being a forcing event for both sides to come to an agreement which would end the shutdown.

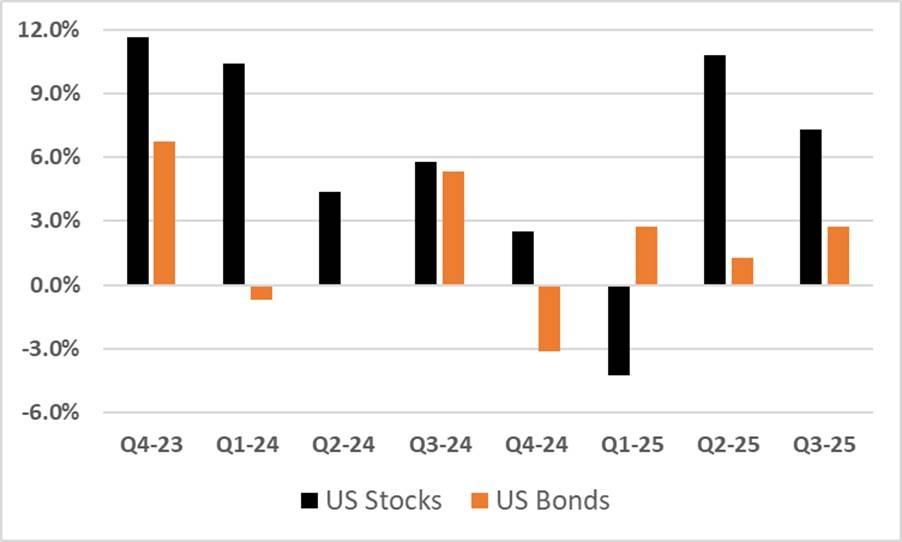

The chart below maps out the nine government shutdowns since 1981 by date and number of days (courtesy of Capital Group).