Government Steps In

Following government actions on Sunday, March 12, a brief press conference was held Monday morning March 13 where President Biden emphasized the following:

- Depositors will be protected

- Investors will not be protected

- No losses will be borne by taxpayers

- The administration will order a full accounting of the situation

- More regulation is likely to follow

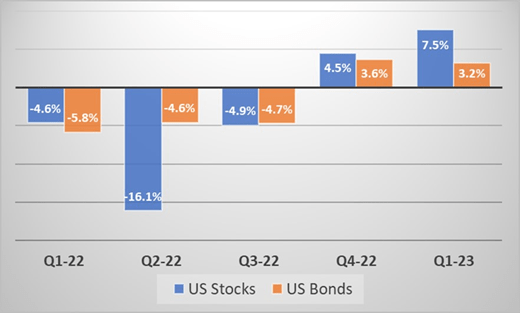

When compared to the Global Financial Crisis of 2008, the current situation has significant differences.

First and foremost, this time government action has been swift, decisive and coordinated. In 2008, it took months for authorities to develop a plan and to act.

Second, the current problem emerged at deposit taking institutions, the issues are transparent, and depositors are being protected.

In 2008, the problems started with real estate lenders and migrated to brokers, and the issues were largely hidden from view or misrepresented for some time. When trouble finally hit retail deposit-taking institutions, the problem had grown so large that the entire financial system was at risk.

Third, investors who hold stocks and bonds of the troubled banks will not be supported, and management of failed companies will be shown the door.

In 2008, part of the ‘solution’ initially was to try to boost stock prices and work with incumbent management teams that had caused the problems.

What actions has the government taken to stem the current crisis?

After taking over Silicon Valley Bank and Signature Bank, the Federal Reserve designated them as systemic risks to the financial system, which gave the Feds authority to backstop uninsured depositors at both institutions. This means people and companies with bank accounts will be able to get their money back in a timely manner.

The Federal Reserve then introduced a new lending facility, called the Bank Term Funding Program, which allows banks to pledge certain assets, like US Treasury bonds, in exchange for loans of up to one year.

This new Fed-run lending facility allows commercially viable banks to avoid selling assets at a loss and helps banks get cash to meet their customers’ demands for their deposits.

Causes of the Crisis

In basic terms, the seeds of the recent bank failures were sown through rapid growth, concentrated customer bases, and shoddy risk management. If you can recall the bank run at Bailey Building and Loan in It’s a Wonderful Life, then you have a reasonable sense of what happened last week.

In the case of Silicon Valley Bank (SVB) and Signature Bank, though, Sam Wainwright wasn’t available to advance the billions of dollars needed to keep the institutions afloat.

SVB seems to be a victim of its own success. SVB developed a niche focus working with technology companies and individuals involved in the tech space. It claimed to have served a majority of US startups.

Following the pandemic, SVB grew like gangbusters, and plowed a lot of its deposits, which are short-term obligations, into relatively safe, but longer-term assets like US Treasuries. It bought Treasuries when interest rates were very low. As interest rates climbed in 2022, bond prices tumbled, and losses mounted for SVB.

When SVB sold a bunch of bonds and realized a large loss last week, customers took notice. When SVB tried to raise fresh capital through a stock offering, investors declined. As herd mentality took hold of the tech crowd that banked at SVB, many demanded their deposits all at once, and the gig was up for SVB.

In addition to customer concentration, SVB depositors tended to keep a lot of money at the bank. At a well-diversified bank, typically half of the deposits are covered by FDIC insurance – the $250,000 deposit guarantee.

In SVB’s case, more than 90% of deposits were above the limit, and therefore uninsured, which made the bank more vulnerable to a run. For Signature Bank, which had niches in the technology sector and the crypto space, nearly 100% of deposits were uninsured.