Stock and bond market performance for the first month of 2025 was pleasing.

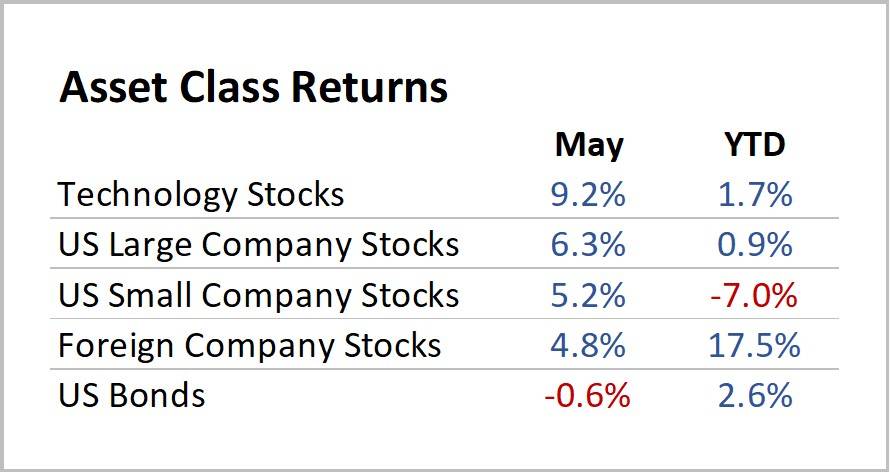

Foreign stocks gained 4.8%, US small company stocks climbed 3.9%, US large company stocks went up 2.7%, and technology shares rose by 2.1%. Bonds were in the black, too: high-quality, intermediate-term debt returned 0.5%.

However, there was turbulence beneath the surface of the stock market, mainly due to developments in the technology sector.

One part of the Artificial Intelligence environment is Large Language Models (LLMs). These AI-powered systems are trained on massive amounts of text data, which facilitate human-like text responses to a wide range of prompts and questions.

ChatGPT is a widely recognized and utilized LLM. It was developed by OpenAI, of which Microsoft holds a minority ownership stake.

All the big tech companies, including Alphabet (Google), Amazon, Apple, Meta (Facebook), Microsoft and Tesla are spending huge amounts of money investing in LLMs and anticipating big future payoffs on this invested capital.

In addition to these well-recognized firms, a constellation of lesser-known US companies (big and small) that supply software, equipment, storage, and energy to support AI initiatives have been riding the AI wave higher.

In mid-January, a new chatbot called DeepSeek caught the attention of tech investors for several reasons: it was developed cheaply; it runs on less-expensive equipment; it is fast; and it is good. Also, its maker is a small Chinese company, not a Silicon Valley behemoth.

Whether or not DeepSeek becomes a true competitive threat to US technology companies is yet to be seen.

But it was a shot fired across the bow of US technology companies, and some US tech stocks swooned for a few days at the end of the month.

Why does this matter for US investors? The main reason is that the US stock market has become more dependent on ever-higher profits, and ever-higher stock prices, from big tech.

The information technology sector has grown from about a quarter of the US stock market a few years ago to more than one-third today.

When the future profitability of US tech companies is called into question, and when tech stocks slip, it’s harder now for stocks in other sectors to pick up the slack.

This also means that even US investors who hold well-diversified portfolios are likely to feel pain if a correction in tech stocks materializes.

In January, tech turbulence was contained to a few days, and stocks generally finished higher at the end of the month.

However, the DeepSeek tremor was a reminder that troubles for technology companies, if sustained, would probably have far reaching effects for all investors.

Regarding the safer side of investing, the “big news” in the bond market for January was: no news.

The Federal Reserve held their first FOMC meeting of 2025, where interest rate policy is reviewed and discussed, and… nothing happened.

Market participants are now expecting the Fed to stand pat for a while, and to keep the target for short-term interest rates steady for the next six months. This contrasts with the “rate cuts” that occurred during the second half of 2024.

Why is no news from the Fed big news?

It likely means savers will continue to enjoy a satisfactory rate of return on their guaranteed money that is kept in high-yield bank savings accounts and bank CDs.

With the lower bound of the Fed Funds target rate at 4.25%, this probably means short-term CDs are likely to provide a 4%+ annual percentage yield (APR) during the first half of 2025.

It also means that the Fed remains vigilant in their fight against inflation.

If the Fed is successful in convincing market participants that inflation is indeed under control, it should translate to a hospitable environment for investors who own intermediate- and longer-term bonds.

With 10-Year Treasuries yielding about 4.5%, it’s reasonable to expect 5%-plus returns for 2025 from bond allocations in investment portfolios, if inflation, and inflation expectations, remain contained in 2025.

But a trade war could be problematic for financial markets.

An emerging risk, especially to the bond market, is a new tariff regime. On February 1, President Trump announced new tariffs on a range of goods coming into the US from Canada, Mexico, and China.

Trade is huge, diverse, and complex, so the ultimate impact of higher duties isn’t easy to know. A lot depends on size, width, and length: how high tariffs go, how broadly they’re applied, and how long they last.

If tariffs come and go quickly, the inflationary impact will be minimal. But a new regime with high tariffs applied to many trade partners that lasts for an extended period could usher in higher inflation.

If expectations about future inflation go up substantially, this will likely mean higher bond yields, with lower prices and lower returns for bonds – especially for intermediate and longer-term bonds and bond funds.

And if history does rhyme (to paraphrase Mark Twain) then resurgent inflation may well prove to be a challenge for stocks, too.

Performance for the month of January is pictured below: